User login

SAN FRANCISCO– The past 18 months may well have been a watershed moment for medical technology in the gastroenterology field, with bullish venture investment in GI med/biotech, Dr. Jay Pasricha said at the 2015 AGA Tech Summit, which is sponsored by the AGA Center for GI Innovation and Technology.

Both small and large companies did well, raising millions in private capital, said Dr. Pasricha of Johns Hopkins University, Baltimore. Several devices moved forward with Food and Drug Administration approval as well.

“I think we have crossed the Rubicon,” he said. “It’s really exciting after years of watching this momentum build. I think GI technology is really going to take off finally, and there is the promise of much more to come.”

The SmartPill food chain perfectly illustrates Dr. Pasricha’s optimistic view. In 2013, Covidien purchased Israel-based Given Imaging for $860 million, acquiring all seven of the company’s product lines, including PillCam, a minimally invasive, nonsedation, optical endoscopy technology that is swallowed to visualize the small bowel, esophagus, and colon; the ManoScan high-resolution manometry technology; Bravo capsule-based pH monitoring; and SmartPill motility monitoring systems.

It didn’t take long for an even bigger fish to join the frenzy. Just this January, Medtronic purchased Covidien for about $50 billion – the largest purchase in medical device history. “The question now, however, is ‘How will it impact us in the GI field in general?’” Dr. Pasricha said.

He outlined three possible scenarios.

“The first, which I fervently hope will happen, is that we finally realize a validation of this space” of GI technologic interventions. “This really does look like the event that will put this field on the map.”

He expressed some hope that the Medtronic purchase will alert big-name surgical device companies to the possibilities inherent in minimally invasive GI interventions. “I hope it will attract key surgical players to the field ,,, shake things up and lead to more research and development, and a rapid advance of technology.”

It took an event like this to set the field’s stars in motion. But dawn hasn’t broken yet, he cautioned.

“It’s also possible that Medtronic will look at the field and decide it really doesn’t like everything in GI, and that it will focus on just a couple of fields, like neuromodulation, at the cost of others.”

The third scenario is the gloomiest, Dr. Pasricha said – although he said it’s probably the least likely.

“It is possible that GI will just turn out to be a speck of dust in Medtronic’s big picture. We’ll just have to wait and see what happens in the next couple of years.”

Overall, 2014 was series of good-news stories for GI med/biotech. The year saw an overall 61% increase in venture capital investments in the arena – nearly $50 billion among 4,356 deals. Nearly $9 billion of this went directly to life science investments, in a 29% jump over 2013. Almost $3 billion was directed to medical device investments – up 27%. Devices in both early- and late-stage development felt the financial love (according to a recent PricewaterhouseCoopers report).

Less invasive GERD interventions fared particularly well last year. A landmark paper demonstrated that Endogastric Solutions’ (San Mateo, Calif.) transoral incisionless fundoplication significantly outperformed medical therapy with proton pump inhibition. EndoGastric Solutions is currently working with the AGA Center for GI Innovation and Technology to collect real-world data evaluating safety, efficacy, and comparative outcomes for this procedure compared with laparoscopic surgery, through the STAR Registry.

EndoStim (Amsterdam) is running a hot race as well – ready to launch a pivotal trial sometime this year. Its implantable device stimulates the lower esophageal sphincter to control reflux. The device is not yet approved for reimbursement in any country. But on March 11, the German Institute for the Hospital Remuneration System granted it a status 1 level, which entitles hospitals to negotiate with payers for at least partial coverage.

All of this activity bodes well for the future, Dr. Pasricha said.

“We have seen GERD procedures come and go now for 15 years. Now the data are really starting to support endoscopic treatment here. I think we are past the inflection point and will see this approach really take over the field.”

The American Medical Association is keeping abreast of all the progress. On March 10, the AMA created a CPT code for transoral incisionless fundoplication. “This will really legitimize this entire field. In 5 years, these techniques may become serious contenders for first-line therapy instead of chronic PPI use. And third-generation therapies will likely emerge to tackle the more difficult cases that are now excluded, like patients with a large hiatal hernia. There’s no question but that transoral is going to be the preferred way of treating GERD.”

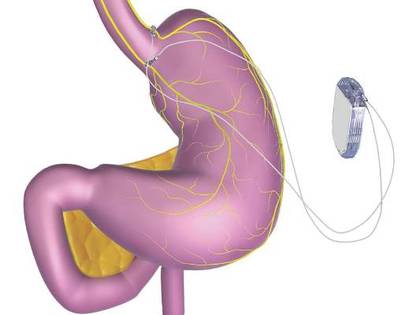

Endoscopy wasn’t the only subspecialty to bask in this new sunny clime. In January, the FDA approved St. Paul–based EnteroMedics’ Maestro system – a neuromodulatory approach to weight loss for obese adults. Maestro is an implanted vagus nerve stimulator that modulates neural signaling, controlling gastric emptying. It also seems to affect hunger signaling, Dr. Pasricha said.

Despite Maestro’s unique method of action – and the fact that it’s the first new weight-loss device approved since 2007 – EnteroMedics’ bottom line hasn’t surged, yet. But it may be too early to look for the impact and in general the outlook for nonsurgical approaches to obesity remains bullish.

Dr. Pasricha reminded the audience about some very basic core principles for successful innovation. “To succeed, you have to have two of three key things. You have to fill an unmet need. The intervention should be simple. And it should be effective.”

Since most GERD patients do fine on medical therapy, those interventions won’t succeed based on need alone. But endoscopic GERD treatments are simple and quite effective. Obesity, on the other hand, presents an enormous unmet need. But the current interventions – including Maestro – are far from simple. And efficacy hasn’t been completely confirmed yet, Dr. Pasricha said.

A couple of other obesity devices are in the works. Apollo Endosurgery (Austin) is focusing on the ORBERA single intragastric balloon. ReShape Medical (San Clemente, Calif.) reported positive data from its pivotal phase III trial of its own intragastric balloon. The device consists of two linked balloons, which the company maintains fit the stomach contours better than does a single balloon.

Over 6 months, patients treated with the dual balloon experienced a mean total body weight loss of 16% (about 17 kg). It seemed to impart some lasting benefit, as those who had continued nutritional counseling after removal maintained about 94% of their weight loss over 7 months of follow-up.

On the basis of these data, ReShape was able to secure close to $7 million in private funding to continue work on the device.

“The great potential for balloon therapy is to make it easier for patients to enter the area of bariatric surgery,” Dr. Pasricha said. “They are not naturally drawn into surgery – they usually have to be pushed into it. But with balloon treatment, they are able to enter, and the threshold for more interventions is then much lower.”

SAN FRANCISCO– The past 18 months may well have been a watershed moment for medical technology in the gastroenterology field, with bullish venture investment in GI med/biotech, Dr. Jay Pasricha said at the 2015 AGA Tech Summit, which is sponsored by the AGA Center for GI Innovation and Technology.

Both small and large companies did well, raising millions in private capital, said Dr. Pasricha of Johns Hopkins University, Baltimore. Several devices moved forward with Food and Drug Administration approval as well.

“I think we have crossed the Rubicon,” he said. “It’s really exciting after years of watching this momentum build. I think GI technology is really going to take off finally, and there is the promise of much more to come.”

The SmartPill food chain perfectly illustrates Dr. Pasricha’s optimistic view. In 2013, Covidien purchased Israel-based Given Imaging for $860 million, acquiring all seven of the company’s product lines, including PillCam, a minimally invasive, nonsedation, optical endoscopy technology that is swallowed to visualize the small bowel, esophagus, and colon; the ManoScan high-resolution manometry technology; Bravo capsule-based pH monitoring; and SmartPill motility monitoring systems.

It didn’t take long for an even bigger fish to join the frenzy. Just this January, Medtronic purchased Covidien for about $50 billion – the largest purchase in medical device history. “The question now, however, is ‘How will it impact us in the GI field in general?’” Dr. Pasricha said.

He outlined three possible scenarios.

“The first, which I fervently hope will happen, is that we finally realize a validation of this space” of GI technologic interventions. “This really does look like the event that will put this field on the map.”

He expressed some hope that the Medtronic purchase will alert big-name surgical device companies to the possibilities inherent in minimally invasive GI interventions. “I hope it will attract key surgical players to the field ,,, shake things up and lead to more research and development, and a rapid advance of technology.”

It took an event like this to set the field’s stars in motion. But dawn hasn’t broken yet, he cautioned.

“It’s also possible that Medtronic will look at the field and decide it really doesn’t like everything in GI, and that it will focus on just a couple of fields, like neuromodulation, at the cost of others.”

The third scenario is the gloomiest, Dr. Pasricha said – although he said it’s probably the least likely.

“It is possible that GI will just turn out to be a speck of dust in Medtronic’s big picture. We’ll just have to wait and see what happens in the next couple of years.”

Overall, 2014 was series of good-news stories for GI med/biotech. The year saw an overall 61% increase in venture capital investments in the arena – nearly $50 billion among 4,356 deals. Nearly $9 billion of this went directly to life science investments, in a 29% jump over 2013. Almost $3 billion was directed to medical device investments – up 27%. Devices in both early- and late-stage development felt the financial love (according to a recent PricewaterhouseCoopers report).

Less invasive GERD interventions fared particularly well last year. A landmark paper demonstrated that Endogastric Solutions’ (San Mateo, Calif.) transoral incisionless fundoplication significantly outperformed medical therapy with proton pump inhibition. EndoGastric Solutions is currently working with the AGA Center for GI Innovation and Technology to collect real-world data evaluating safety, efficacy, and comparative outcomes for this procedure compared with laparoscopic surgery, through the STAR Registry.

EndoStim (Amsterdam) is running a hot race as well – ready to launch a pivotal trial sometime this year. Its implantable device stimulates the lower esophageal sphincter to control reflux. The device is not yet approved for reimbursement in any country. But on March 11, the German Institute for the Hospital Remuneration System granted it a status 1 level, which entitles hospitals to negotiate with payers for at least partial coverage.

All of this activity bodes well for the future, Dr. Pasricha said.

“We have seen GERD procedures come and go now for 15 years. Now the data are really starting to support endoscopic treatment here. I think we are past the inflection point and will see this approach really take over the field.”

The American Medical Association is keeping abreast of all the progress. On March 10, the AMA created a CPT code for transoral incisionless fundoplication. “This will really legitimize this entire field. In 5 years, these techniques may become serious contenders for first-line therapy instead of chronic PPI use. And third-generation therapies will likely emerge to tackle the more difficult cases that are now excluded, like patients with a large hiatal hernia. There’s no question but that transoral is going to be the preferred way of treating GERD.”

Endoscopy wasn’t the only subspecialty to bask in this new sunny clime. In January, the FDA approved St. Paul–based EnteroMedics’ Maestro system – a neuromodulatory approach to weight loss for obese adults. Maestro is an implanted vagus nerve stimulator that modulates neural signaling, controlling gastric emptying. It also seems to affect hunger signaling, Dr. Pasricha said.

Despite Maestro’s unique method of action – and the fact that it’s the first new weight-loss device approved since 2007 – EnteroMedics’ bottom line hasn’t surged, yet. But it may be too early to look for the impact and in general the outlook for nonsurgical approaches to obesity remains bullish.

Dr. Pasricha reminded the audience about some very basic core principles for successful innovation. “To succeed, you have to have two of three key things. You have to fill an unmet need. The intervention should be simple. And it should be effective.”

Since most GERD patients do fine on medical therapy, those interventions won’t succeed based on need alone. But endoscopic GERD treatments are simple and quite effective. Obesity, on the other hand, presents an enormous unmet need. But the current interventions – including Maestro – are far from simple. And efficacy hasn’t been completely confirmed yet, Dr. Pasricha said.

A couple of other obesity devices are in the works. Apollo Endosurgery (Austin) is focusing on the ORBERA single intragastric balloon. ReShape Medical (San Clemente, Calif.) reported positive data from its pivotal phase III trial of its own intragastric balloon. The device consists of two linked balloons, which the company maintains fit the stomach contours better than does a single balloon.

Over 6 months, patients treated with the dual balloon experienced a mean total body weight loss of 16% (about 17 kg). It seemed to impart some lasting benefit, as those who had continued nutritional counseling after removal maintained about 94% of their weight loss over 7 months of follow-up.

On the basis of these data, ReShape was able to secure close to $7 million in private funding to continue work on the device.

“The great potential for balloon therapy is to make it easier for patients to enter the area of bariatric surgery,” Dr. Pasricha said. “They are not naturally drawn into surgery – they usually have to be pushed into it. But with balloon treatment, they are able to enter, and the threshold for more interventions is then much lower.”

SAN FRANCISCO– The past 18 months may well have been a watershed moment for medical technology in the gastroenterology field, with bullish venture investment in GI med/biotech, Dr. Jay Pasricha said at the 2015 AGA Tech Summit, which is sponsored by the AGA Center for GI Innovation and Technology.

Both small and large companies did well, raising millions in private capital, said Dr. Pasricha of Johns Hopkins University, Baltimore. Several devices moved forward with Food and Drug Administration approval as well.

“I think we have crossed the Rubicon,” he said. “It’s really exciting after years of watching this momentum build. I think GI technology is really going to take off finally, and there is the promise of much more to come.”

The SmartPill food chain perfectly illustrates Dr. Pasricha’s optimistic view. In 2013, Covidien purchased Israel-based Given Imaging for $860 million, acquiring all seven of the company’s product lines, including PillCam, a minimally invasive, nonsedation, optical endoscopy technology that is swallowed to visualize the small bowel, esophagus, and colon; the ManoScan high-resolution manometry technology; Bravo capsule-based pH monitoring; and SmartPill motility monitoring systems.

It didn’t take long for an even bigger fish to join the frenzy. Just this January, Medtronic purchased Covidien for about $50 billion – the largest purchase in medical device history. “The question now, however, is ‘How will it impact us in the GI field in general?’” Dr. Pasricha said.

He outlined three possible scenarios.

“The first, which I fervently hope will happen, is that we finally realize a validation of this space” of GI technologic interventions. “This really does look like the event that will put this field on the map.”

He expressed some hope that the Medtronic purchase will alert big-name surgical device companies to the possibilities inherent in minimally invasive GI interventions. “I hope it will attract key surgical players to the field ,,, shake things up and lead to more research and development, and a rapid advance of technology.”

It took an event like this to set the field’s stars in motion. But dawn hasn’t broken yet, he cautioned.

“It’s also possible that Medtronic will look at the field and decide it really doesn’t like everything in GI, and that it will focus on just a couple of fields, like neuromodulation, at the cost of others.”

The third scenario is the gloomiest, Dr. Pasricha said – although he said it’s probably the least likely.

“It is possible that GI will just turn out to be a speck of dust in Medtronic’s big picture. We’ll just have to wait and see what happens in the next couple of years.”

Overall, 2014 was series of good-news stories for GI med/biotech. The year saw an overall 61% increase in venture capital investments in the arena – nearly $50 billion among 4,356 deals. Nearly $9 billion of this went directly to life science investments, in a 29% jump over 2013. Almost $3 billion was directed to medical device investments – up 27%. Devices in both early- and late-stage development felt the financial love (according to a recent PricewaterhouseCoopers report).

Less invasive GERD interventions fared particularly well last year. A landmark paper demonstrated that Endogastric Solutions’ (San Mateo, Calif.) transoral incisionless fundoplication significantly outperformed medical therapy with proton pump inhibition. EndoGastric Solutions is currently working with the AGA Center for GI Innovation and Technology to collect real-world data evaluating safety, efficacy, and comparative outcomes for this procedure compared with laparoscopic surgery, through the STAR Registry.

EndoStim (Amsterdam) is running a hot race as well – ready to launch a pivotal trial sometime this year. Its implantable device stimulates the lower esophageal sphincter to control reflux. The device is not yet approved for reimbursement in any country. But on March 11, the German Institute for the Hospital Remuneration System granted it a status 1 level, which entitles hospitals to negotiate with payers for at least partial coverage.

All of this activity bodes well for the future, Dr. Pasricha said.

“We have seen GERD procedures come and go now for 15 years. Now the data are really starting to support endoscopic treatment here. I think we are past the inflection point and will see this approach really take over the field.”

The American Medical Association is keeping abreast of all the progress. On March 10, the AMA created a CPT code for transoral incisionless fundoplication. “This will really legitimize this entire field. In 5 years, these techniques may become serious contenders for first-line therapy instead of chronic PPI use. And third-generation therapies will likely emerge to tackle the more difficult cases that are now excluded, like patients with a large hiatal hernia. There’s no question but that transoral is going to be the preferred way of treating GERD.”

Endoscopy wasn’t the only subspecialty to bask in this new sunny clime. In January, the FDA approved St. Paul–based EnteroMedics’ Maestro system – a neuromodulatory approach to weight loss for obese adults. Maestro is an implanted vagus nerve stimulator that modulates neural signaling, controlling gastric emptying. It also seems to affect hunger signaling, Dr. Pasricha said.

Despite Maestro’s unique method of action – and the fact that it’s the first new weight-loss device approved since 2007 – EnteroMedics’ bottom line hasn’t surged, yet. But it may be too early to look for the impact and in general the outlook for nonsurgical approaches to obesity remains bullish.

Dr. Pasricha reminded the audience about some very basic core principles for successful innovation. “To succeed, you have to have two of three key things. You have to fill an unmet need. The intervention should be simple. And it should be effective.”

Since most GERD patients do fine on medical therapy, those interventions won’t succeed based on need alone. But endoscopic GERD treatments are simple and quite effective. Obesity, on the other hand, presents an enormous unmet need. But the current interventions – including Maestro – are far from simple. And efficacy hasn’t been completely confirmed yet, Dr. Pasricha said.

A couple of other obesity devices are in the works. Apollo Endosurgery (Austin) is focusing on the ORBERA single intragastric balloon. ReShape Medical (San Clemente, Calif.) reported positive data from its pivotal phase III trial of its own intragastric balloon. The device consists of two linked balloons, which the company maintains fit the stomach contours better than does a single balloon.

Over 6 months, patients treated with the dual balloon experienced a mean total body weight loss of 16% (about 17 kg). It seemed to impart some lasting benefit, as those who had continued nutritional counseling after removal maintained about 94% of their weight loss over 7 months of follow-up.

On the basis of these data, ReShape was able to secure close to $7 million in private funding to continue work on the device.

“The great potential for balloon therapy is to make it easier for patients to enter the area of bariatric surgery,” Dr. Pasricha said. “They are not naturally drawn into surgery – they usually have to be pushed into it. But with balloon treatment, they are able to enter, and the threshold for more interventions is then much lower.”